What is Global Dog Nutrition Supplements Market?

The global dog nutrition supplements market is a rapidly growing sector within the pet care industry, driven by increasing awareness among pet owners about the health and well-being of their canine companions. These supplements are designed to provide essential nutrients that may not be sufficiently available in regular dog food, thereby supporting overall health, enhancing immunity, and addressing specific health concerns such as joint health, skin and coat condition, and digestive health. The market encompasses a wide range of products, including vitamins, minerals, fatty acids, probiotics, and other specialized formulations tailored to meet the diverse needs of dogs at different life stages. As pet ownership continues to rise globally, with more people treating their pets as family members, the demand for high-quality, effective nutritional supplements is expected to grow. This trend is further supported by advancements in veterinary science and increased consumer access to information about pet health, leading to more informed purchasing decisions. The market is characterized by a variety of players, from established pet food manufacturers to specialized companies focusing solely on pet supplements, all striving to innovate and offer products that cater to the evolving needs of pet owners and their beloved dogs.

Chewable Tablets, Liquids & Gels, Powders in the Global Dog Nutrition Supplements Market:

Chewable tablets, liquids and gels, and powders are among the most popular forms of dog nutrition supplements available in the global market, each offering unique benefits and catering to different preferences of pet owners and their dogs. Chewable tablets are particularly favored for their convenience and ease of administration. They often come in flavors that appeal to dogs, making them more like a treat than a supplement, which can be especially helpful for dogs that are picky eaters or resistant to taking pills. These tablets are typically formulated to address specific health concerns, such as joint support, skin and coat health, or digestive issues, and are designed to be palatable and easy to chew, ensuring that dogs receive the full benefit of the active ingredients. Liquids and gels, on the other hand, offer a versatile option for pet owners who may have difficulty administering tablets to their dogs. These forms can be easily mixed with food or administered directly into the dog's mouth, providing a stress-free experience for both the pet and the owner. Liquids and gels are often used for supplements that require precise dosing, such as omega-3 fatty acids or certain vitamins, allowing for easy adjustment based on the dog's size and specific needs. Powders are another popular form of dog nutrition supplements, offering flexibility in administration and formulation. They can be easily sprinkled over food or mixed into wet food, making them an ideal choice for dogs that are sensitive to changes in texture or flavor. Powders are often used for supplements that target overall health and wellness, such as multivitamins or probiotics, and can be formulated to include a wide range of nutrients in a single product. This form is particularly beneficial for pet owners looking to provide comprehensive nutritional support without having to administer multiple products. Each of these forms of dog nutrition supplements has its own set of advantages, and the choice often depends on the specific needs of the dog, the preferences of the owner, and the health goals they are aiming to achieve. As the global dog nutrition supplements market continues to expand, manufacturers are likely to continue innovating and developing new formulations and delivery methods to meet the evolving needs of pet owners and their dogs.

Puppies, Adult Dogs in the Global Dog Nutrition Supplements Market:

The usage of global dog nutrition supplements varies significantly between puppies and adult dogs, as each life stage has distinct nutritional requirements and health considerations. For puppies, nutrition supplements play a crucial role in supporting growth and development. During the early stages of life, puppies require a balanced intake of essential nutrients to support the rapid growth of bones, muscles, and organs. Supplements that provide calcium, phosphorus, and other vital minerals are often recommended to ensure proper skeletal development and prevent conditions such as rickets. Additionally, omega-3 fatty acids, particularly DHA, are important for brain development and cognitive function, making them a valuable addition to a puppy's diet. Probiotics and digestive enzymes can also be beneficial for puppies, as they help establish a healthy gut microbiome and support efficient digestion, which is essential for nutrient absorption and overall health. For adult dogs, the focus of nutrition supplements often shifts towards maintaining health and preventing age-related issues. Joint health supplements, such as glucosamine and chondroitin, are commonly used to support mobility and alleviate symptoms of arthritis or joint pain, which can become more prevalent as dogs age. Antioxidants, such as vitamins C and E, are also popular supplements for adult dogs, as they help combat oxidative stress and support immune function. Additionally, supplements that promote skin and coat health, such as omega-6 fatty acids and biotin, are often used to address issues like dry skin, itching, or dull coats. For both puppies and adult dogs, the choice of supplements should be guided by the specific needs of the individual dog, taking into consideration factors such as breed, size, activity level, and any existing health conditions. Consulting with a veterinarian is always recommended to ensure that the chosen supplements are appropriate and beneficial for the dog's overall health and well-being. As the global dog nutrition supplements market continues to grow, pet owners have access to an ever-expanding range of products designed to support the health and happiness of their canine companions at every stage of life.

Global Dog Nutrition Supplements Market Outlook:

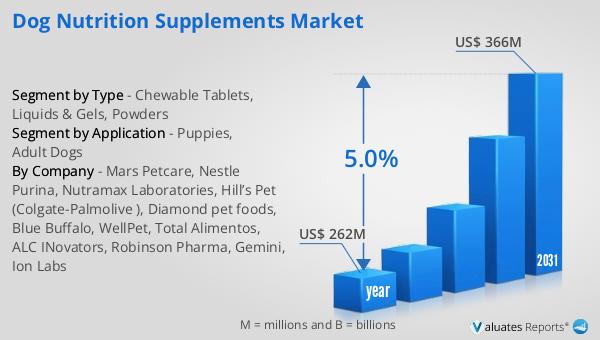

The global market for dog nutrition supplements was valued at $262 million in 2024 and is anticipated to grow to a revised size of $366 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.0% over the forecast period. This growth is indicative of the increasing emphasis on pet health and wellness, as more pet owners seek to provide their dogs with the best possible care. In the United Kingdom, for instance, annual spending on veterinary and other pet services has surged from £2.6 billion in 2015 to £4 billion in 2021, marking a significant 54% increase over six years. This trend underscores the growing willingness of pet owners to invest in their pets' health, including nutrition supplements. Furthermore, according to Vetnosis, the global animal health industry was projected to increase by 12% to $38.3 billion in 2021, highlighting the expanding market for products that support animal well-being. In China, the pet medical market was estimated to be around 67.5 billion yuan, accounting for approximately 22.5% of the entire pet industry, as per the 2022 China Pet Medical Industry White Paper. This data reflects the substantial market potential for dog nutrition supplements, driven by rising pet ownership and the increasing recognition of the importance of preventive health care for pets. As the market continues to evolve, manufacturers and retailers are likely to focus on innovation and product development to meet the diverse needs of pet owners and their dogs.

| Report Metric | Details |

| Report Name | Dog Nutrition Supplements Market |

| Accounted market size in year | US$ 262 million |

| Forecasted market size in 2031 | US$ 366 million |

| CAGR | 5.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Mars Petcare, Nestle Purina, Nutramax Laboratories, Hill’s Pet (Colgate-Palmolive ), Diamond pet foods, Blue Buffalo, WellPet, Total Alimentos, ALC INovators, Robinson Pharma, Gemini, Ion Labs |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |