What is LED Die Bonding Adhesive - Global Market?

LED Die Bonding Adhesive is a specialized material used in the assembly of LED components, playing a crucial role in the electronics industry. This adhesive is essential for attaching the LED die, which is the semiconductor light source, to the substrate or package. The global market for LED Die Bonding Adhesive is driven by the increasing demand for LEDs in various applications, such as lighting, displays, and automotive sectors. As LEDs become more prevalent due to their energy efficiency and long lifespan, the need for reliable and effective bonding solutions grows. These adhesives must provide excellent thermal and electrical conductivity, ensuring the LED functions optimally while maintaining durability and stability. The market is characterized by continuous innovation, with manufacturers striving to develop adhesives that offer better performance, ease of application, and environmental compliance. As industries increasingly adopt LED technology, the demand for high-quality die bonding adhesives is expected to rise, making it a dynamic and evolving market.

Epoxy Die Bonding Adhesive, Silicone Die Bonding Adhesive in the LED Die Bonding Adhesive - Global Market:

Epoxy Die Bonding Adhesive and Silicone Die Bonding Adhesive are two primary types of adhesives used in the LED Die Bonding Adhesive market. Epoxy adhesives are known for their strong bonding capabilities and excellent thermal and chemical resistance. They are widely used in applications where durability and reliability are paramount. Epoxy adhesives provide a robust bond that can withstand harsh environmental conditions, making them ideal for outdoor LED applications and automotive lighting. Their ability to maintain structural integrity under thermal cycling and mechanical stress is a significant advantage in the LED industry. On the other hand, Silicone Die Bonding Adhesives offer flexibility and excellent thermal stability. They are particularly useful in applications where thermal management is critical, such as high-power LED modules. Silicone adhesives can accommodate the thermal expansion and contraction of materials, reducing the risk of stress and potential damage to the LED components. This flexibility also makes them suitable for applications requiring a degree of movement or vibration, such as in automotive or aerospace industries. Both epoxy and silicone adhesives are integral to the LED Die Bonding Adhesive market, each offering unique properties that cater to specific application needs. The choice between epoxy and silicone adhesives often depends on the specific requirements of the LED application, including factors such as operating temperature, environmental conditions, and mechanical stress. Manufacturers in the LED industry must carefully consider these factors when selecting the appropriate adhesive to ensure optimal performance and longevity of their products. As the demand for LEDs continues to grow, the development of advanced adhesive solutions that meet the evolving needs of the industry remains a key focus for manufacturers. Innovations in adhesive technology are expected to drive the market forward, offering new opportunities for growth and expansion.

LED Display, LED Backlight in the LED Die Bonding Adhesive - Global Market:

LED Die Bonding Adhesive plays a vital role in the production and performance of LED displays and LED backlights. In LED displays, these adhesives are used to attach the LED die to the substrate, ensuring a secure and reliable connection. The adhesive must provide excellent thermal and electrical conductivity to maintain the performance and longevity of the display. As LED displays are used in a wide range of applications, from televisions and computer monitors to digital signage and billboards, the demand for high-quality die bonding adhesives is significant. These adhesives must withstand various environmental conditions, including temperature fluctuations and humidity, to ensure the display's reliability and durability. In LED backlights, die bonding adhesives are crucial for attaching the LED die to the backlight unit, which is used in devices such as smartphones, tablets, and laptops. The adhesive must provide a strong bond while allowing for efficient heat dissipation to prevent overheating and ensure optimal performance. As the demand for thinner and more energy-efficient devices grows, the need for advanced die bonding adhesives that can meet these requirements is increasing. The global market for LED Die Bonding Adhesive is driven by the growing adoption of LED technology in various applications, with displays and backlights being key areas of focus. Manufacturers are continually developing new adhesive solutions to meet the evolving needs of the industry, offering improved performance, reliability, and environmental compliance. As the market continues to expand, the demand for high-quality die bonding adhesives is expected to rise, providing new opportunities for growth and innovation.

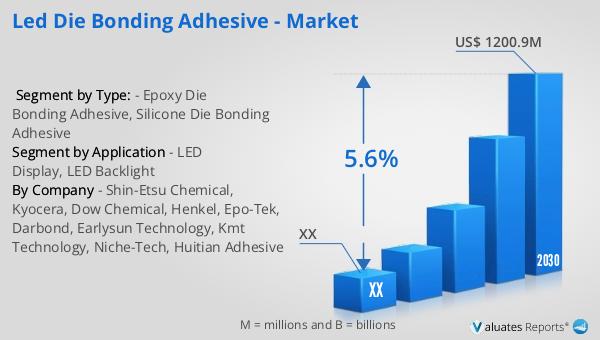

LED Die Bonding Adhesive - Global Market Outlook:

In 2023, the global market for LED Die Bonding Adhesive was valued at approximately $817 million. It is projected to grow to a revised size of around $1,200.9 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.6% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for LED technology across various sectors, driving the need for effective bonding solutions. The North American market, in particular, is expected to see significant growth, although specific figures for this region were not provided. The anticipated expansion of the market underscores the importance of LED Die Bonding Adhesive in supporting the widespread adoption of LED technology. As industries continue to embrace LEDs for their energy efficiency and long lifespan, the demand for reliable and high-performance adhesives is likely to increase. This growth presents opportunities for manufacturers to innovate and develop new adhesive solutions that meet the evolving needs of the market. The projected market expansion highlights the critical role of LED Die Bonding Adhesive in the electronics industry and its potential for future growth.

| Report Metric | Details |

| Report Name | LED Die Bonding Adhesive - Market |

| Forecasted market size in 2030 | US$ 1200.9 million |

| CAGR | 5.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Shin-Etsu Chemical, Kyocera, Dow Chemical, Henkel, Epo-Tek, Darbond, Earlysun Technology, Kmt Technology, Niche-Tech, Huitian Adhesive |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |