What is Global Wet Electronic Chemicals for Integrated Circuits Market?

The Global Wet Electronic Chemicals for Integrated Circuits Market is a specialized sector within the chemical industry, focusing on the production and supply of essential chemicals used in the manufacturing of integrated circuits (ICs). These chemicals are crucial for various stages of IC fabrication, including cleaning, etching, and doping processes that help in building the microscopic structures of silicon chips. The market caters to a wide range of chemicals, including acids, solvents, bases, and photoresist chemicals, each serving a specific purpose in the intricate process of semiconductor manufacturing. As the demand for smaller, faster, and more efficient electronic devices continues to grow, so does the need for high-purity wet electronic chemicals. These chemicals are vital for achieving the precision and cleanliness required in the semiconductor fabrication process, making them indispensable for the production of integrated circuits found in virtually all electronic devices today. The market's growth is propelled by advancements in technology and the expanding electronics industry, highlighting its critical role in the modern digital age.

General Wet Electronic Chemicals, Functional Wet Electronic Chemicals in the Global Wet Electronic Chemicals for Integrated Circuits Market:

General Wet Electronic Chemicals and Functional Wet Electronic Chemicals are two broad categories within the Global Wet Electronic Chemicals for Integrated Circuits Market, each playing a pivotal role in the semiconductor manufacturing process. General wet electronic chemicals include a variety of solvents, acids, and bases used primarily for cleaning and preparing silicon wafers, ensuring they are free of any contaminants before the intricate process of circuit patterning begins. These chemicals are the backbone of the semiconductor manufacturing process, providing the necessary purity and consistency required for high-quality IC production. On the other hand, Functional Wet Electronic Chemicals are specialized chemicals used in specific steps of IC fabrication, such as doping, etching, and photoresist application. These chemicals are designed to perform precise functions, including altering the electrical properties of silicon wafers, creating the tiny patterns that form the basis of integrated circuits, and developing the photoresist material that guides the etching process. The demand for both general and functional wet electronic chemicals is driven by the relentless pursuit of smaller, more complex, and more efficient integrated circuits, necessitating continuous advancements in chemical formulations and purity levels. As the semiconductor industry evolves, so does the complexity and specificity of the chemicals required, underscoring the critical role these materials play in enabling the technological leaps seen in consumer electronics, computing, and telecommunications.

Consumer Electronics, Semiconductor, Photovoltaic Solar, LED in the Global Wet Electronic Chemicals for Integrated Circuits Market:

The Global Wet Electronic Chemicals for Integrated Circuits Market finds its applications across various dynamic and fast-growing sectors, including Consumer Electronics, Semiconductor, Photovoltaic Solar, and LED industries. In the realm of Consumer Electronics, these chemicals are indispensable for the production of high-performance, compact, and reliable integrated circuits that power a myriad of devices, from smartphones to laptops and wearable technology. The precision and purity of wet electronic chemicals ensure the functionality and longevity of these devices, making them integral to the consumer electronics supply chain. Within the Semiconductor industry, wet electronic chemicals are at the heart of the fabrication process, enabling the creation of semiconductors that are the foundational components of all electronic devices. Their role in cleaning, etching, and doping processes is critical for the production of high-quality semiconductors that meet the industry's stringent standards. The Photovoltaic Solar sector relies on these chemicals for the manufacturing of solar cells, where they are used to clean and texture the silicon wafers, enhancing the efficiency of light absorption and conversion into electricity. Lastly, in the LED industry, wet electronic chemicals are used in the etching processes that shape the light-emitting diodes, crucial for producing bright and energy-efficient lighting solutions. The widespread usage of these chemicals across such diverse sectors underscores their importance in the advancement of modern technology and sustainable energy solutions.

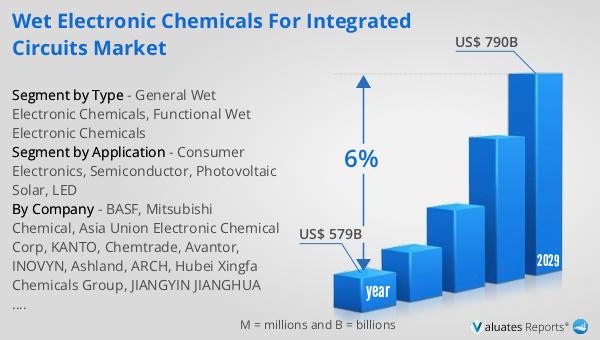

Global Wet Electronic Chemicals for Integrated Circuits Market Outlook:

The market outlook for the semiconductor industry presents a promising future, with the sector's value estimated at US$ 579 billion in 2022, and projections indicating a growth to US$ 790 billion by 2029. This growth trajectory, expected to unfold at a compound annual growth rate (CAGR) of 6% during the forecast period, underscores the robust demand and ongoing expansion within the industry. Such growth is reflective of the increasing reliance on semiconductor technology across various sectors, including consumer electronics, automotive, and industrial applications, driven by advancements in technology and the digital transformation of economies worldwide. The semiconductor market's expansion is a testament to the critical role these components play in the modern world, powering everything from simple electronic devices to complex systems that form the backbone of the digital economy. This outlook not only highlights the financial growth of the sector but also points to the increasing importance of semiconductor technology in driving innovation and enabling the development of new products and services that will shape the future of the global economy.

| Report Metric | Details |

| Report Name | Wet Electronic Chemicals for Integrated Circuits Market |

| Accounted market size in year | US$ 579 billion |

| Forecasted market size in 2029 | US$ 790 billion |

| CAGR | 6% |

| Base Year | year |

| Forecasted years | 2024 - 2029 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | BASF, Mitsubishi Chemical, Asia Union Electronic Chemical Corp, KANTO, Chemtrade, Avantor, INOVYN, Ashland, ARCH, Hubei Xingfa Chemicals Group, JIANGYIN JIANGHUA MICRO-ELECTRONIC MATERIALS, Grandit, Jiangsu Denoir Technology, Dow Chemical Company, Zhejiang Kaisn Fluorochemical, Crystal Clear Electronic Material |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |