What is Global Polypropylene Melt Blown Nonwoven Fabrics Market?

The Global Polypropylene Melt Blown Nonwoven Fabrics Market is a significant segment within the textile industry, primarily due to its versatile applications and unique properties. Polypropylene melt blown nonwoven fabrics are created through a process where polymer melt is extruded through small nozzles surrounded by high-speed blowing gas, resulting in fine fibers that form a web-like structure. This process gives the fabric its distinctive characteristics, such as high filtration efficiency, softness, and lightweight nature. These fabrics are extensively used in various industries, including healthcare, automotive, and home textiles, due to their ability to provide excellent barrier properties and breathability. The market for these fabrics is driven by increasing demand for personal protective equipment, especially in the wake of global health crises, and the growing awareness of hygiene and safety standards. Additionally, advancements in manufacturing technologies and the development of eco-friendly variants are expected to further propel the market's growth. The Asia-Pacific region is a major player in this market, owing to its robust manufacturing capabilities and expanding industrial base. Overall, the Global Polypropylene Melt Blown Nonwoven Fabrics Market is poised for steady growth, driven by its diverse applications and the continuous evolution of consumer needs.

Net Weight Below 25 (g/m2), Net Weight 25-50 (g/m2), Net Weight Above 50 (g/m2) in the Global Polypropylene Melt Blown Nonwoven Fabrics Market:

In the Global Polypropylene Melt Blown Nonwoven Fabrics Market, the net weight of the fabric plays a crucial role in determining its application and performance characteristics. Fabrics with a net weight below 25 grams per square meter (g/m2) are typically used in applications where lightweight and high breathability are essential. These fabrics are often employed in the production of disposable hygiene products, such as diapers and sanitary napkins, where comfort and air permeability are critical. The low weight ensures that the products are not bulky, providing ease of use and comfort to the end-users. On the other hand, fabrics with a net weight ranging from 25 to 50 g/m2 strike a balance between strength and softness, making them suitable for applications that require moderate durability and flexibility. These fabrics are commonly used in medical and industrial applications, such as surgical masks, gowns, and filtration systems, where a combination of barrier protection and comfort is necessary. The intermediate weight allows for effective filtration while maintaining user comfort, which is crucial in environments where prolonged use is required. Fabrics with a net weight above 50 g/m2 are designed for applications that demand high strength and durability. These heavier fabrics are used in more demanding industrial applications, such as automotive interiors, geotextiles, and heavy-duty filtration systems. The increased weight provides enhanced mechanical properties, making them suitable for use in environments where the fabric is subjected to significant stress and wear. The choice of net weight is a critical consideration for manufacturers and end-users alike, as it directly impacts the performance and suitability of the fabric for specific applications. As the market continues to evolve, manufacturers are focusing on developing innovative solutions that cater to the diverse needs of various industries, ensuring that the right balance of weight, strength, and functionality is achieved. This focus on innovation is driving the development of new products and technologies that enhance the performance of polypropylene melt blown nonwoven fabrics, further expanding their range of applications. The ongoing advancements in manufacturing processes and material science are expected to lead to the creation of fabrics with improved properties, such as enhanced filtration efficiency, increased durability, and reduced environmental impact. These developments are likely to open up new opportunities for the use of polypropylene melt blown nonwoven fabrics in emerging applications, such as advanced filtration systems, smart textiles, and sustainable packaging solutions. As the demand for high-performance materials continues to grow, the Global Polypropylene Melt Blown Nonwoven Fabrics Market is well-positioned to meet the evolving needs of industries and consumers worldwide.

Hygiene, Industrial, Home Textile, Cloths, Automotive, Protective Mask, Others in the Global Polypropylene Melt Blown Nonwoven Fabrics Market:

The usage of Global Polypropylene Melt Blown Nonwoven Fabrics Market spans across various sectors, each benefiting from the unique properties of these fabrics. In the hygiene sector, these fabrics are integral to the production of disposable products like diapers, sanitary napkins, and adult incontinence products. Their high absorbency, softness, and breathability make them ideal for ensuring comfort and hygiene. In the industrial sector, polypropylene melt blown nonwoven fabrics are used in filtration systems, protective clothing, and insulation materials. Their ability to filter out particles and provide thermal insulation makes them valuable in environments where safety and efficiency are paramount. In home textiles, these fabrics are used in products like mattress covers, pillowcases, and furniture linings, where their lightweight and durable nature enhances comfort and longevity. In the clothing industry, they are used in the production of interlinings and insulation materials, providing warmth without adding bulk. The automotive sector utilizes these fabrics in interior components, such as seat covers and cabin filters, where their durability and filtration properties contribute to vehicle comfort and performance. One of the most significant applications of polypropylene melt blown nonwoven fabrics is in the production of protective masks. The COVID-19 pandemic has highlighted the importance of these fabrics in manufacturing masks that offer high filtration efficiency and breathability, protecting individuals from airborne particles and pathogens. Beyond these specific applications, polypropylene melt blown nonwoven fabrics are also used in a variety of other areas, including agriculture, construction, and packaging. Their versatility and adaptability make them suitable for a wide range of uses, from crop protection covers to geotextiles and packaging materials. As industries continue to seek materials that offer a combination of performance, cost-effectiveness, and sustainability, the demand for polypropylene melt blown nonwoven fabrics is expected to grow. Manufacturers are increasingly focusing on developing eco-friendly variants and enhancing the performance characteristics of these fabrics to meet the evolving needs of consumers and industries. The ongoing advancements in material science and manufacturing technologies are likely to lead to the development of new applications and markets for polypropylene melt blown nonwoven fabrics, further driving their adoption across various sectors.

Global Polypropylene Melt Blown Nonwoven Fabrics Market Outlook:

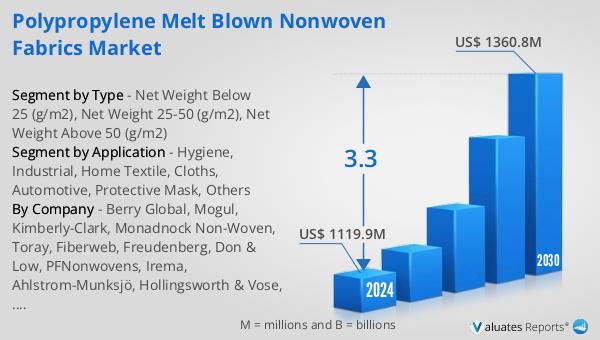

The global market for Polypropylene Melt Blown Nonwoven Fabrics was valued at approximately $1,153 million in 2024, with projections indicating it could reach around $1,443 million by 2031, growing at a compound annual growth rate (CAGR) of 3.3% over the forecast period. The Asia-Pacific region stands out as the largest market for these fabrics, accounting for about 60% of global sales. This dominance is largely due to the region's strong manufacturing capabilities and expanding industrial base. Following Asia-Pacific, North America and Europe hold significant market shares of approximately 20% and 16%, respectively. These regions benefit from well-established healthcare sectors and stringent environmental standards, which drive the demand for high-quality nonwoven fabrics. Leading companies in this industry include Berry Global, Mogul, Kimberly-Clark, Monadnock Non-Woven, Ahlstrom-Munksjö, and Sinopec. The top three players collectively hold around 12% of the market, indicating a competitive landscape with opportunities for growth and innovation. As the market continues to evolve, companies are focusing on developing advanced products and expanding their presence in emerging markets to capitalize on the growing demand for polypropylene melt blown nonwoven fabrics.

| Report Metric | Details |

| Report Name | Polypropylene Melt Blown Nonwoven Fabrics Market |

| Accounted market size in year | US$ 1153 million |

| Forecasted market size in 2031 | US$ 1443 million |

| CAGR | 3.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Berry Global, Mogul, Kimberly-Clark, Monadnock Non-Woven, Toray, Fiberweb, Freudenberg, Don & Low, PFNonwovens, Irema, Ahlstrom-Munksjo, Hollingsworth & Vose, Guoen Holdings, CHTC Jiahua Nonwoven, JOFO, TEDA Filter, Yanjiang Group, Zisun Technology, Ruiguang Group, Xinlong Group, Shandong Laifen Nonwovens, Kunshan Huaxinhong Nonwoven Technology, Jinchun Co., Ltd., KNH Enterprise, Nanliu Enterprise |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |